Committee Blog: Defining Legal Hemp – It Isn’t Always Simple Math

By: Todd Glider, Chief Business Development Officer, MobiusPay Inc.

Contributing Authors: Paul Dunford, Green Check Verified | Shawn Kruger, Avivatech | Kameron Richards, Kameron Richards Esq.

Produced by: NCIA’s Banking & Financial Services Committee

If you are a cannabis-related business, and are looking to accept credit cards, it is only possible to do so if you are selling a product that is defined as legal hemp by the 2018 Farm Bill.

The 2018 Farm Bill provides that:

“The term ‘hemp’ means the plant Cannabis sativa L. and any part of that plant, including the seeds thereof and all derivatives, extracts, cannabinoids, isomers, acids, salts, and salts of isomers, whether growing or not, with a delta-9 tetrahydrocannabinol concentration of not more than 0.3 percent on a dry weight basis.”

For the most part, it’s pretty cut-and-dry. Marijuana is a schedule 1 drug. Hemp is not. If your product has less than .3% Delta-9 on a dry weight basis, it’s not marijuana, it’s hemp. And since it’s hemp, it’s federally legal. And since it’s federally legal, it can be purchased with checks, credit cards, or debit cards. Hemp products are, reductively, as incendiary as a stick of butter.

Of course, there is the law and there is how acquiring banks—banks that offer merchant accounts—interpret the law. Across the U.S., there are hundreds of acquiring banks. Of those, only six or seven offer merchant accounts to hemp businesses.

That’s it, plus payment service provider Square.

The immediate problem for the few acquiring banks that have, laudably, said, “Yes,” to hemp is, “how do we distinguish products that are .3% Delta-9 or less (and therefore, yawningly legal) from those that are over .3% Delta-9 (and therefore, illegal as angel dust)?”

Enter the Certificate of Analysis, or COA, or lab report. While there is nothing in the law stating that COAs are required to prove that a product is within the federally legal limit, their role is sacrosanct during the boarding process. For every hemp-derived product, there must be a corresponding COA proving that the product being sold is hemp, and not marijuana.

Fortunately, there are labs across the nation. The U.S. Department of Agriculture website lists 85, as of May 2023. Manufacturers and businesses ship their samples to these labs. The labs run their tests and the COAs are issued.

Simple, right?

Not really.

There are no standards in place for these reports. No templates. Every laboratory’s COAs—while substantively providing the same information—look a little different. Furthermore, most bankers haven’t seen a lab report since high school chemistry, and you’ve got a recipe for confusion or misunderstanding (frequently both).

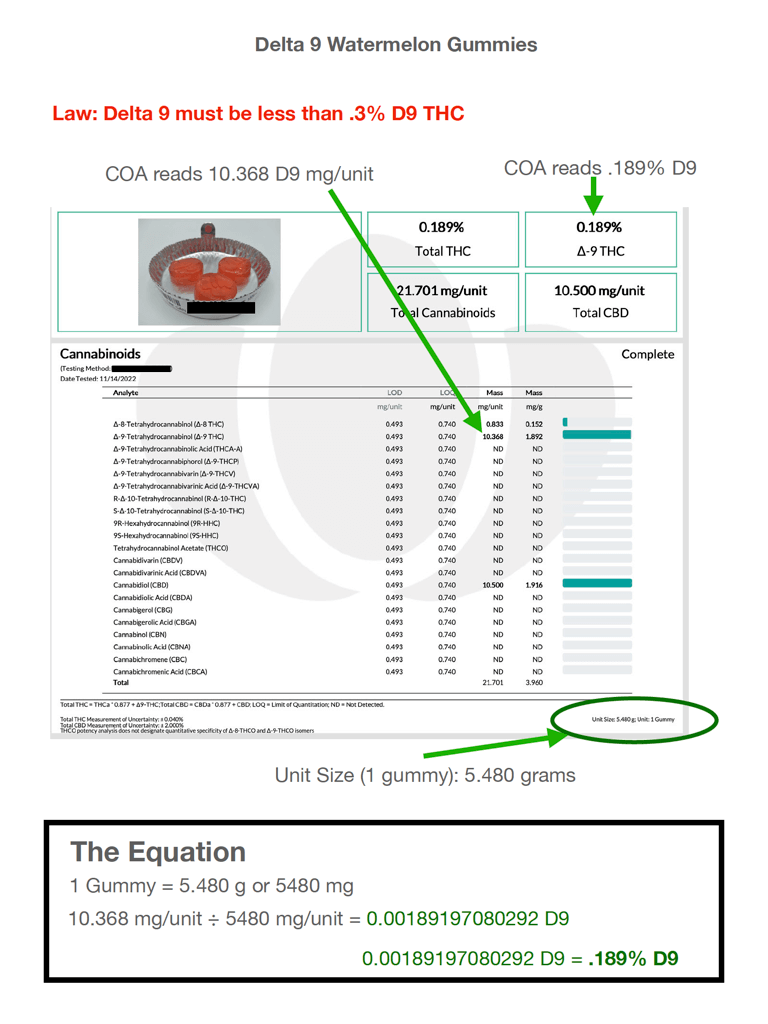

This COA, when it was initially presented to the bank, was rejected. To the underwriter, it was an open and shut case.

When the bank opened its door to offering acquiring to hemp businesses, its policy was to reject anything with greater than .3% Delta-9 by weight.

The top of this COA showed an instance of Delta 9 that read .189%. That passed muster, certainly. However, when he delved further into the analyte detail, he noted additional Delta-9 figures in excess of the .3% limit:

- 10.368 in the mg/unit cell

- 1.892 in the mg/g cell

It was not clear to the bank’s underwriter which of the two—per-unit or per-gram—corresponded with the by-weight percentage he was to be mindful of, but both were certainly over the .3% limit.

So, open and shut case: DECLINED

The salesperson that brought the merchant to this bank was surprised by the rejection. He hadn’t looked at the COAs very closely, but it seemed unlikely that this merchant had been selling products on her website that were in excess of .3% Delta-9.

Why? Because if the merchant had been selling products on its website in excess of .3% Delta-9, it would have been engaging in egregious felony drug trafficking. The salesperson doubted that was the case.

The salesperson did something he didn’t normally do: he took out his calculator.

He wanted to know why it read .189% Delta 9 at the top, but 10.368 in the analyte table. He noted the unit size at the bottom of the page was a gummy weighing 5.480g.

For the sake of simplicity, he multiplied that by 1000 to convert it to milligrams. That made it 5480 mg

Then he entered the onerous 10.368mg from the mg/unit figure in the analyte table and divided it by 5480mg. The resulting calculation netted the following total: .0018919.

Next, he converted it to a percent, and found that the result was .189%, which matched the figure at the top of the COA, exactly.

The next day, the salesperson presented the COA to the bank, with the markings and The Equation just as shown here.

It was an open and shut case: ACCEPTED

This situation is an example of why banks and credit unions unknowingly reject compliant hemp businesses from merchant processing solutions. As stated, a simple mathematical calculation was the difference between being accepted or rejected for necessary merchant processing services. Without proper merchant servicing not only are cannabis businesses’ profitability affected because they can only take cash; cash is also not as traceable or auditable as electronic transactions.

In general, businesses providing services to the cannabis industry are often challenged with disentangling legal risks with the benefits of their necessary services providing more transparency. With enhanced knowledge of the cannabis industry and its parameters, the cannabis industry will recognize a greater participation by all businesses necessary for the life of the industry thereby enhancing cannabis businesses’ likelihood to succeed but also enhancing the legitimacy and regulation of the industry.

Member Blog: Payment Processing in the Cannabis Space – Part 3

by Todd Glider, MobiusPay, Inc

This is Part III in a series of blog posts entitled Payment Processing in the Cannabis Space. Click here for Part I, and here, for Part II.

It would be naive to suggest that the cannabis retailer isn’t also facing headwinds resulting, simply, from a century of bad press. Putting the questions of federal vs state legality aside, it’s important to note that payments and banking issues are not unique to the plant-touchers, or Cannabis-Related Business Tier I, or CRB Tier I. CRB Tier II, the ancillary, or cannabis-adjacent businesses, have challenges of their own.

On any given day, there are a galaxy of companies, consultancies, medical practices, and professional organizations expanding their reach into our growth industry. And why not? The legalization of cannabis is a bona fide 100-year event, and intrepid business owners of all shapes and sizes sense opportunity, a new market for their wares and expertise.

And while they may be welcomed with open arms by their new colleagues and contemporaries in the cannabis community, they often find their banking relationships suddenly souring.

A message from their payment processor arrives.

It says, “Sorry, Gayle Force Grow Lights. Your processing has been suspended.”

A message from their bank hits the Inbox.

It says, “Sorry, Gayle Force Grow Lights. Your account is being shutdown down.”

These are chilling, but easily explainable events. And while it may be tempting to tuck them neatly into a dystopian ‘Big Brother is Watching You’ framework, what’s happening here is more Kafkaesque bureaucracy than Orwellian totalitarianism.

So what happened? Gayle Force Grow Lights has been marketing its grow lights to the people of Maine for 25 years. Gayle, the owner, saw cannabis legalization sweeping the nation, and thought, “Here is a new market for my grow lights.”

She updates her digital storefront accordingly, which is to say, she added a new marketing bullet: Ideal for cannabis cultivators.

To us, the word ‘cannabis,’ is an industry term. In Gayle Force Grow Lights’ case, it is marketing jargon. However, to the processors and banks employing dummy algorithms to crawl their clients’ sites, that word is a red flag. When that red flag is tripped, Gayle’s processing is suspended. When that red flag is tripped, Gayle’s business bank account is shut down.

Gayle Force Grow Lights, in the eyes of the PSP it’s been using to accept credit cards, and in the eyes of the financial institution it’s been using to bank, has, suddenly, transitioned from a reliably safe client to a potentially risky client.

Risky clients need to be watched more closely. Risky clients require more due diligence and KYC measures. And since it is not cost-effective for a PSP with 24 million accounts — or a bank with 70 million clients — to police Gayle Force Grow Lights, which processes $100,000 in transactions per-month, and has an average cash balance of $2 million, they show Gayle, and her small business, the door.

The good news? Gayle Force Grow Lights is fictitious. I made it up.

The bad news? Gayle Force Grow Lights is a composite. This is happening to businesses in the cannabis space every day.

What Does the Future Hold?

Right now, merchant accounts are only an option for sellers of hemp and hemp derivatives. But the day will come, with national legalization, when every cannabis-related retailer will have the legal option of accepting credit cards.

As with CBD, it is inevitable that there will be numerous challenges to merchants when this occurs. It is inevitable that cannabis sales will be deemed ‘high risk’ by the card associations. It is inevitable, also, that only a handful of Acquiring Banks will elect to throw their hats into the ring.

The good news is that it is just as inevitable that the companies providing merchant accounts for CBD businesses today will be the ones providing merchant accounts to businesses selling THC in excess of .3%, tomorrow. As always, the most dependable among them will be those that have direct relationships with the Acquiring Banks. This will ensure that account acquisition and maintenance for all cannabis-related businesses is as smooth and as easy as it can be.

MobiusPay, Inc. is a US-based global financial services organization that is committed to empowering individuals and businesses. For more than a dozen years, MobiusPay has leveraged state-of-the-art secure billing technology, long-standing relationships with financial institutions and award-winning customer support to provide merchant processing and payment solutions to brick-and-mortar and digital businesses around the world.

MobiusPay, Inc. is a US-based global financial services organization that is committed to empowering individuals and businesses. For more than a dozen years, MobiusPay has leveraged state-of-the-art secure billing technology, long-standing relationships with financial institutions and award-winning customer support to provide merchant processing and payment solutions to brick-and-mortar and digital businesses around the world.

Todd Glider has been an e-Commerce leader since the start of the Internet age. He has an MFA in Creative Writing from the University of Miami, and has served as CEO for small and medium-sized technology companies in Spain, Austria and the United States. As our Chief Business Development Officer, Todd introduces MobiusPay’s suite of award-winning financial services to new industries, and implements the development strategies and key partnerships needed to bring value to new customers.

Member Blog: Payment Processing In The Cannabis Space

by Todd Glider, MobiusPay, Inc

There is a lot of confusion about payment processing in the cannabis space because payment processing is somewhat confusing to begin with, and because, in the cannabis space, ambiguity is a way of life.

The title of this very blog post could, realistically, seem misleading to some.

So, to be clear, when I say, “Cannabis Space,” I mean the entire industry — from plant-touchers (CBD included) to the ancillary businesses built up around it.

The passage of the 2018 Farm Bill marked an exciting new chapter for the industry. Suddenly, CBD, or, more specifically, any ingestible cannabis product containing .3% THC or less by volume, was classified as hemp. And since it is marijuana, and not hemp, that is defined as a Schedule I substance under the United States Controlled Substance Act, the Farm Bill, technically, made products like CBD as legal as cow milk — federally, anyway.

The upshot of this new classification is that now, at least some players in the cannabis space can market their products to a national base of consumers and clients, and they can do so by accepting credit cards as payment.

However, the myriad Acquiring Banks across the United States have not exactly jumped for joy at the prospect of providing credit card processing in the form of merchant accounts to CBD retailers. Reticence rules. CBD is considered high risk, and four years on, only a handful of them have thrown their hat in the ring.

Jargon Alert I: Acquiring Banks and Issuing Banks

In merchant processing parlance, banks fall into two categories: Acquiring Banks and Issuing Banks. Acquiring Banks, or, Acquirers, provide merchant processing accounts to businesses wishing to accept credit card transactions. Issuing Banks, short for Card Issuing Banks, are banks that offer branded payment cards directly to consumers. For example, if your bank has ever offered you a Visa card, it is an Issuing Bank (not that it couldn’t also be an Acquiring Bank, too).

Jargon Alert II: CBD is ‘High Risk’

CBD is deemed high risk by the card associations (i.e., Visa, MasterCard, American Express), and when the card associations deem a product or industry high risk, most Acquiring Banks tap out. This is because financial institutions are, by nature, risk averse (subprime mortgage crisis notwithstanding).

So let’s talk for a minute about risk. High risk, that compound term, is a truncation of a longer phrase: ‘Higher risk of fraud or chargebacks.’

Why are CBD products at higher risk of fraud? It’s impossible to say for sure since the Visas and MasterCards of the world are publicly traded companies with their own trade secrets and IP, but there are several characteristics unique to CBD, or any cannabis product now federally legal, that likely figured into that decision.

Those FDA disclaimers that CBD retailers must print or paste on all product packaging and webpages are as good a place as any to start. They are mandatory because none of the benefits assigned to CBD have been clinically proven. There just isn’t enough data or testing at this point, and no big story there. That’s what happens when you demonize a plant for 100 years.

Consequently, from the perspective of the FDA, and the card associations, by extension, consumers are making CBD purchases with baked-in expectations based, exclusively, on word-of-mouth advice and anecdotal data. That’s a recipe for dissatisfied customers. And dissatisfied customers tend to charge back transactions.

The card associations, and the banks who provide merchant accounts, worry incessantly about fraud and chargebacks.

Too Close for Comfort

Dissatisfied customers aside, there are onerous legal nuances that make the prospect of boarding cannabis merchants, even those selling products that are federally legal, daunting for banks.

Selling a product with .31% THC across state lines is felonious. It is a federal offense. Violating a law like that could get a bank’s charter revoked, or, at a minimum, result in massive fines.

On the other hand, selling a product with .30% THC across state lines is 100% federally legal. As stated above, safe as milk, federally.

That is a heck of a distinction. If any product contains more than .3% THC by volume, it is ‘marijuana’ in the eyes of the federal government. From the perspective of the banks, that’s a little close for comfort. Furthermore, banks don’t operate laboratories. They must rely on testing data presented to them in the form of third-party lab reports — Certificates of Analysis or COAs for short — to verify that the products being sold are federally legal.

The last thing an Acquiring Bank wants to do is violate a federal law EVER. It could result in a loss of their charter, lawsuits, and massive fines. And it’s important to keep in mind that the Acquiring Banks out there offering merchant accounts to CBD retailers are not giant, publicly traded institutions like Bank of America or Wells Fargo. They tend to be much smaller, and therefore, have infinitely smaller war chests for court cases.

Still, separating the federally legal Tier I cannabis product from the federally illegal Tier I cannabis product should be pretty cut-and-dry. If the product you’re selling is .3% THC by volume or less, it is exempt from the Controlled Substance Act (CSA). If that threshold is documented in the product’s Certificates of Analysis (COA), you ought to be able to sell it.

Unfortunately, it’s not that simple. When bank underwriters look at percentages of Delta 8, Delta 9, and Delta 10 on the COAs that cross their desks, they’re frequently at sixes and sevens trying to figure the whole thing out.

From the perspective of the 2018 Farm Bill, a cannabis product is hemp if it contains .3% Delta-9 THC or less by volume, but what everybody says is “.3% THC or less by volume.” Consequently, when the compliance officer at the bank is performing her due diligence by inspecting the COAs corresponding to each product, she may encounter a lot of crooked numbers, and she may blanch at the results.

Those results, often, look something like the following:

00.195% D9-THC

52.475% d8-THC.

Federally, the Delta-9 threshold is the only threshold that matters. The 2018 Farm Bill says as much, and the 9th Circuit Court of Appeals in California affirmed it in a ruling this past May. Therefore, in the example above, the Delta-9 threshold has not been crossed. It’s not even close. It is textbook HEMP, even if the Delta-8 threshold is off the charts.

However, if the compliance officer was provided the remit, “.3% or lower,” he’s likely to look at this and say, “Fail,” without realizing that the Delta-8 THC information is irrelevant as far as federal law goes.

Complicating the underwriting further is the fact that there is, to date, no standard template for COA reports. Every lab presents them differently. Bank compliance officers rarely moonlight as scientists. Like most of us, these CBD COAs are probably the first lab reports they’ve looked at since high school chemistry.

Furthermore, the banks can set their own rules. They don’t have to board CBD merchants. Few do, and those few that do have their own standards and practices.

Todd Glider has been an e-Commerce leader since the start of the Internet age. He has an MFA in Creative Writing from the University of Miami, and has served as CEO for small and medium-sized technology companies in Spain, Austria and the United States. As our Chief Business Development Officer, Todd introduces MobiusPay’s suite of award-winning financial services to new industries, and implements the development strategies and key partnerships needed to bring value to new customers.

MobiusPay, Inc. is a U.S.-based global financial services organization that is committed to empowering individuals and businesses. For more than a dozen years, MobiusPay has leveraged state-of-the-art secure billing technology, long-standing relationships with financial institutions and award-winning customer support to provide merchant processing and payment solutions to brick and mortar and digital businesses around the world.

Follow NCIA

Newsletter

Facebook

Twitter

LinkedIn

Instagram

News & Resource Topics

–

This Just In

Member Blog: The Evolving Cannabis Legal & Regulatory Landscape in 2026

How THCa Vapes Are Changing Consumer