Member Blog: “What are companies like us doing?” – Revisiting compensation peer groups

by Fred Whittlesey, Cannabis Compensation Consultants

Central to most discussions about executive compensation – not unlike any business discussion – is the question “what are other companies doing?” In compensation analyses, this guides the selection of data, typically for companies of a similar size in the same industry. Inherent in this approach is that a list of companies defines the landscape of business competitors, including competition for talent. Boards of Directors want to know – and are required to know – marketplace norms, trends, and practices as elements of their approving executive compensation.

Executive compensation in peer companies provides a guideline for determining appropriate pay levels and program design – what the other companies are doing. But these groups are typically determined by business-based characteristics – revenue, market cap, industry code, etc. In the rapidly evolving cannabis sector, these criteria may not yield a meaningful comparison group.

Most importantly, no data from a talent competitor aspect is typically included as a metric, though companies mention “talent competitors” as a criterion for inclusion in their “peer group” as we call it.

Peer Group Pressure

Proxy advisory firms (e.g., ISS, Glass Lewis) encourage and provide specific guidelines for the development of peer groups for executive compensation comparisons among public companies. In fact, they not only prefer but expect this process and disclosure. But their process may not make sense for every company as it focuses on market cap, revenue size, and industry code.

The problem for cannabis companies is:

- There is no industry classification code for cannabis companies (with the exception of some suppliers that may serve multiple industries)

- Most cannabis companies have not disclosed benchmarking peers

- Size constraints are moot when #1 and #2 don’t exist.

And, none of this peer selection process gets to the root of the purpose: Identifying talent competitors to help guide the design of compensation programs to attract valuable employees from those competitors and keep employees from defecting to those competitors.

Complexities of a Cannabis Peer Group

Some of the largest cannabis companies are issuing proxy statements that parallel the norms for large mature companies in the U.S. For a cannabis company, constructing a peer group is a challenge given the characteristics of vertical integration of the business, merger and acquisition activity, and – most importantly – the breadth of occupational categories represented by these firms’ employees.

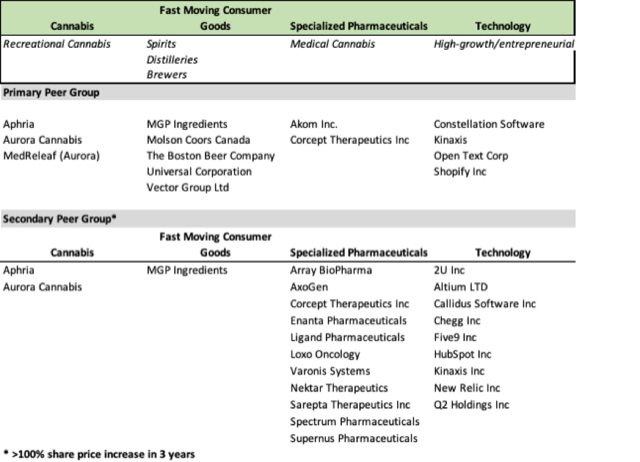

Here, for example, is the peer group disclosed by Canopy Growth – two sets of companies from four industry sectors – cannabis, fast moving consumer goods, specialized pharmaceuticals, and technology:

This is the most complex peer group structure I have seen among the hundreds and hundreds of companies’ disclosures I have reviewed.

The cannabis sector poses this challenge: Covering some or all of the subspecialties that are under one roof with a group of similar companies, when there may be no similar companies

Some Recent Examples

“High Times… hires President”

“Cannabis producer Tilray taps ex-Molson, Revlon employees for Executive roles”

When Tilray or High Times recruits for executive positions, who are their “talent competitors” as recruiting targets? Tilray does not disclose a peer group in its latest SEC filing that would require disclosure of such.

Interestingly, Molson Coors, Pharmaca, Revlon, Goldman Sachs, GE, and Apple have never included a cannabis company as one of their peers. That is likely because Tilray (drug manufacturers – specialty and generic) and High Times (not a public company) would not fit the criteria for those companies’ peer groups.

-

- The peer group disclosed by Revlon (household and personal products) includes Hain Celestial (packaged goods), Clorox (household and personal products), and Tupperware Brands (packaging and containers).

-

- Molson Coors’ peer group includes The Hershey Company (confectioners) and J.M Smucker Company (packaged foods).

Yet Molson Coors, Revlon, and other non-cannabis companies are rapidly losing executives to cannabis companies – the definition of talent competitors.

Let’s Try Peering Backwards

Maybe the current process is backwards. As cannabis companies face a limited supply of talent with cannabis experience, they will find the talent from diverse industries and then, perhaps, compile a list the companies from where those new executives came. That would indeed be a talent competitor peer group.

What would that look like? Based on publicly-available information about the previous employer of the executives in these cannabis companies, we can “peer backwards” into what their cannabis-relevant talent pool looks like.

What About Your Company?

Your company – in the cannabis sector – is hiring a new C-level executive, maybe even a CEO. Your company did not disclose a peer group because it has not thought about a peer group. Your company is vertically integrated – cultivation, extraction, distribution, branding, retail – so it is simply a matter of finding a candidate with experience in all of those, or some of those…or one of those?

Let’s continue “peering backwards” – looking at where executives have come from and having a compensation program that keeps our company off of the next company’s “from” list.

What would that look like? Based on publicly-available information about the previous employer of the executives in these cannabis companies, we can “peer backwards” into what their cannabis-relevant talent pool looks like:

Peering Backwards

| Company | CEO | CFO |

| Tilray | Silicon Valley Bank (SVB) | Primo Water Corporation |

| Canopy Growth | Constellation Brands

Montana Mills |

Gallo Winery

Pepsico |

| Charlotte’s Web | Kellogg Company | Crocs

Orbitz |

Financial services, water dispensers, consumer products, bakeries, wine, soda and snacks, cereal, shoes, travel – not the usual mix of talent sources.

Cannabis Companies Finding Their Tribe

One will hear that the cannabis sector is in the “Wild West” phase, which is sort of like saying that a 14-year old is in the Wild West phase of adulthood. The only norms appearing are those carried over by the large consulting firms accustomed to consulting to mature companies. The entrepreneurial companies in the cannabis sector need not worry about self-appointed third-party opinions of their executive compensation practices – until they grow up. They can pursue practices that make sense for their business strategy, talent sourcing strategy, dispersion of locations, and other business-driven factors.

As we research executive compensation in the cannabis sector, we find a blend of compensation practices from these diverse industries, defying the notion that there is a “norm” or a “median” in the cannabis sector. Understanding executive pay in cannabis companies, for now, requires understanding executive pay in perhaps dozens of industries.

As cannabis companies grow, they will face the need for some additional structure and processes around executive compensation. But many of these companies are, and will continue to be, Smaller Reporting Companies, Emerging Growth Companies, Controlled Companies, TSX-V listed, or in another category with lesser disclosure requirements and lesser pressure from proxy advisers and institutional shareholders. With more of a grassroots shareholder base, they will have more maneuvering room in compensation design, less concern about the “optics” of a given executive compensation action or program, and more opportunities for the compensation program to fit the business, not fit a third-party’s unsolicited opinion of compensation. This is already leading to greater creativity and innovation in compensation design among cannabis companies.

Fred Whittlesey is the founder and President of Compensation Venture Group, SPC (CVG) – a Washington Social Purpose Corporation – operates as Cannabis Compensation ConsultantsTM and maintains a database of cannabis companies’ peer groups, executive pay levels, and executive hire sources. Fred Whittlesey is the founder and President of CVG, and with more than 35 years of experience in compensation, has worked for hundreds or companies across the industries that collectively comprise the cannabis sector – agriculture, biopharma, retail, distribution, manufacturing, marketing, branding, REITs, financial services, and technology.

Fred Whittlesey is the founder and President of Compensation Venture Group, SPC (CVG) – a Washington Social Purpose Corporation – operates as Cannabis Compensation ConsultantsTM and maintains a database of cannabis companies’ peer groups, executive pay levels, and executive hire sources. Fred Whittlesey is the founder and President of CVG, and with more than 35 years of experience in compensation, has worked for hundreds or companies across the industries that collectively comprise the cannabis sector – agriculture, biopharma, retail, distribution, manufacturing, marketing, branding, REITs, financial services, and technology.

Follow NCIA

Newsletter

Facebook

Twitter

LinkedIn

Instagram

News & Resource Topics

–

This Just In

NCIA Applauds Reintroduction of SAFE Banking Following Lobby Days

Beyond Rescheduling: Inside NCIA’s 14th Annual National Cannabis Industry Lobby Days